Customer loyalty can seem like an unattainable goal in the auto industry. Understanding the factors that drive loyalty rates helps keep current customers and even attract new ones.

It’s also important to have insights into why customer preferences can change. For example, today’s sports-car enthusiast could become tomorrow’s minivan dad.

Customers easily can move from dealership to dealership, segment to segment and brand to brand. The average household car-make loyalty rate across all segments is just 54.1%.

But one industry segment, certified pre-owned vehicles, quietly but consistently outperforms the average.

While CPO vehicles long have been regarded as a way to move high-quality, low-mileage off-lease used units, they also can stimulate significant customer loyalty.

Experian analyzed nearly 12.6 million return-to-market events at the automotive retail level and found consumers going from one CPO vehicle to another from the same automaker had a loyalty rate of 75%. No other transition came close, as shown below.

• New vehicle to new vehicle, 60.9%.

• CPO to new vehicle, 54.1%.

• New vehicle to CPO vehicle, 49.1%.

• Non-CPO used vehicle to CPO, 47.1%.

What’s driving these high CPO loyalty rates? It’s a combination of higher consumer confidence, lower cost, vehicle availability and the ability of the manufacturer to manage these aspects to their advantage and to their dealers’ advantage.

First, manufacturer inspection programs and relative affordability have always been the hallmark of successful CPO programs. The inspection programs boost consumer confidence in vehicle quality. The lower cost opens availability to customers across a larger segment of incomes and credit tiers.

The second key is managing the available supply. As any good economist will say, ample supply is the key to keeping cost low. Increases in leasing in recent years hold the key to maintaining a healthy supply of CPO vehicles, and this should continue in the coming years.

In the third quarter of 2015, leasing accounted for 26.9% of all new-vehicle transactions. This jumped to 29.49% a year later.

As these vehicles come off lease, they create a significant supply of potential CPO vehicles. Since the average lease term is 36 months, CPO supply looks good through at least 2019.

Monthly budget often drives purchase decisions. As long as monthly payments for new-vehicle loans remain high, it’s likely the lease-to-CPO cycle will continue.

Many shoppers buy based on what fits their monthly budget. In the third quarter of 2016, the average payment for a new-vehicle loan was $495, while the average monthly payment for a lease was $405. That $90-per-month savings is attractive to many consumers.

Likewise, the average payment for a used-vehicle loan was $375 in the same period. While CPO vehicles are lower mileage than most used vehicles, their payments still are far more manageable than the typical new-vehicle loan. This combination of affordability and availability is likely to keep CPO vehicles at the forefront of consumer purchase decisions.

Who is winning CPO loyalty?

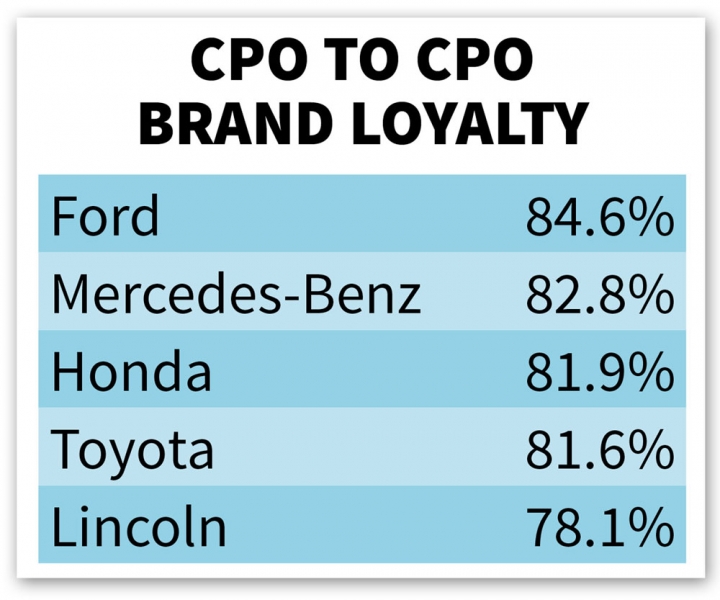

Some manufacturers are already doing a remarkable job of building loyalty through their CPO programs. Ford, for example, has successfully placed both Ford and Lincoln among the industry’s top five brands for CPO-to-CPO loyalty:

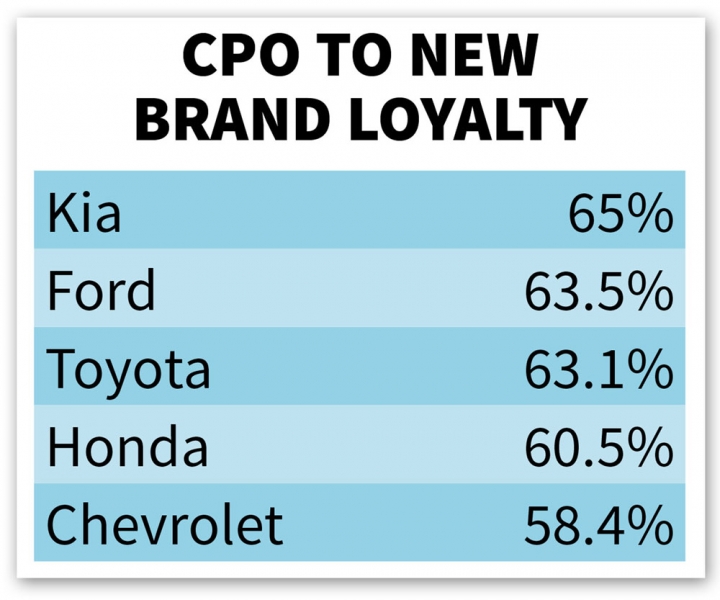

When it comes to converting CPO customers to new-vehicle customers, Kia is in the lead, with Ford coming in a close second.

Automakers continue to increase sales through higher rates of lease penetration, then channeling these off-lease vehicles into CPO fleets. In essence, they are controlling both supply and demand of their off-lease used vehicles and building an amazingly loyal customer base.

By understanding these loyalty rates, manufacturers, dealers and remarketers make smarter decisions that create more opportunities for themselves and in-market consumers.

Brad Smith is Experian’s director of Automotive Market Insights and Product Management.